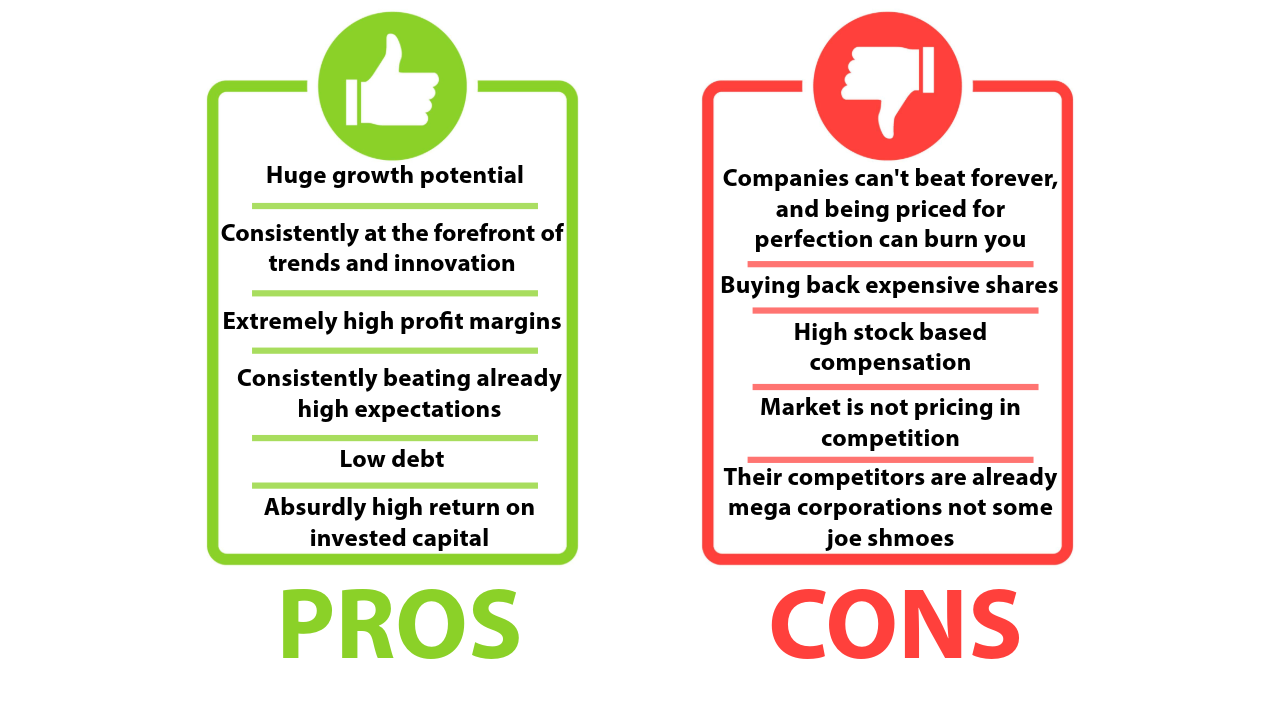

With NVDA being up ~90% year to date and over 2,000% over the past 5 years, many retail investors say this stock is a must-have in any long-term portfolio. Unfortunately, using past stock performance to justify future returns is not how real investing is actually done. In fact, usually when a stock rises parabolically, its future returns are low for a while or even negative. As Benjamin Graham said, "“In the short run, the market is a voting machine. In the long run, it is a weighing machine.”

Over time, the company's fundamentals drive the stock's price. So, let's dive into NVDA's fundamentals and see what's going on here...

Analysis | Price Targets

Analysis

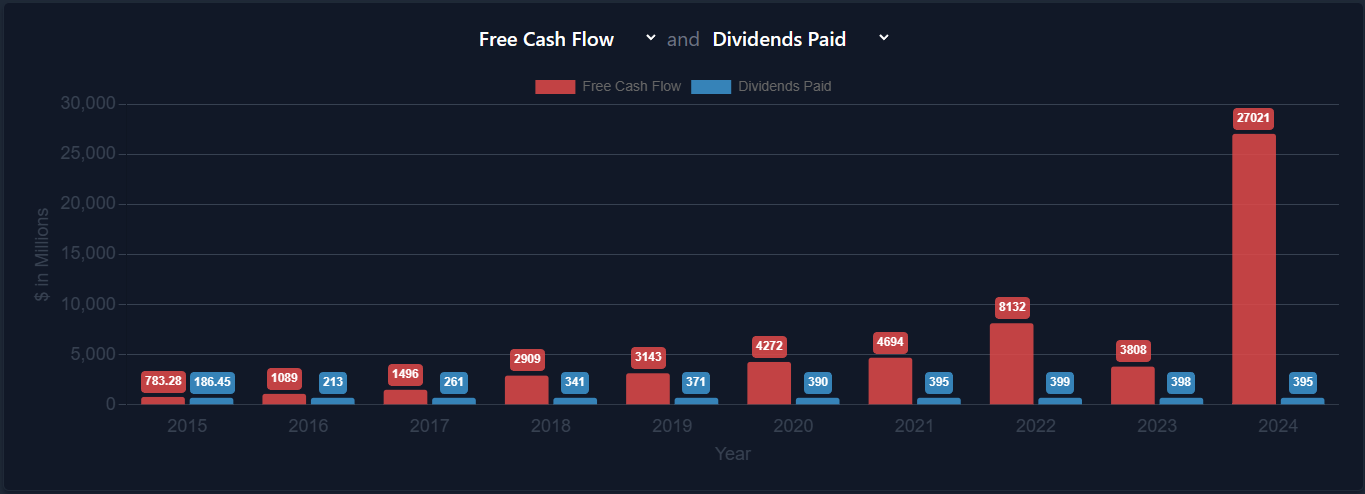

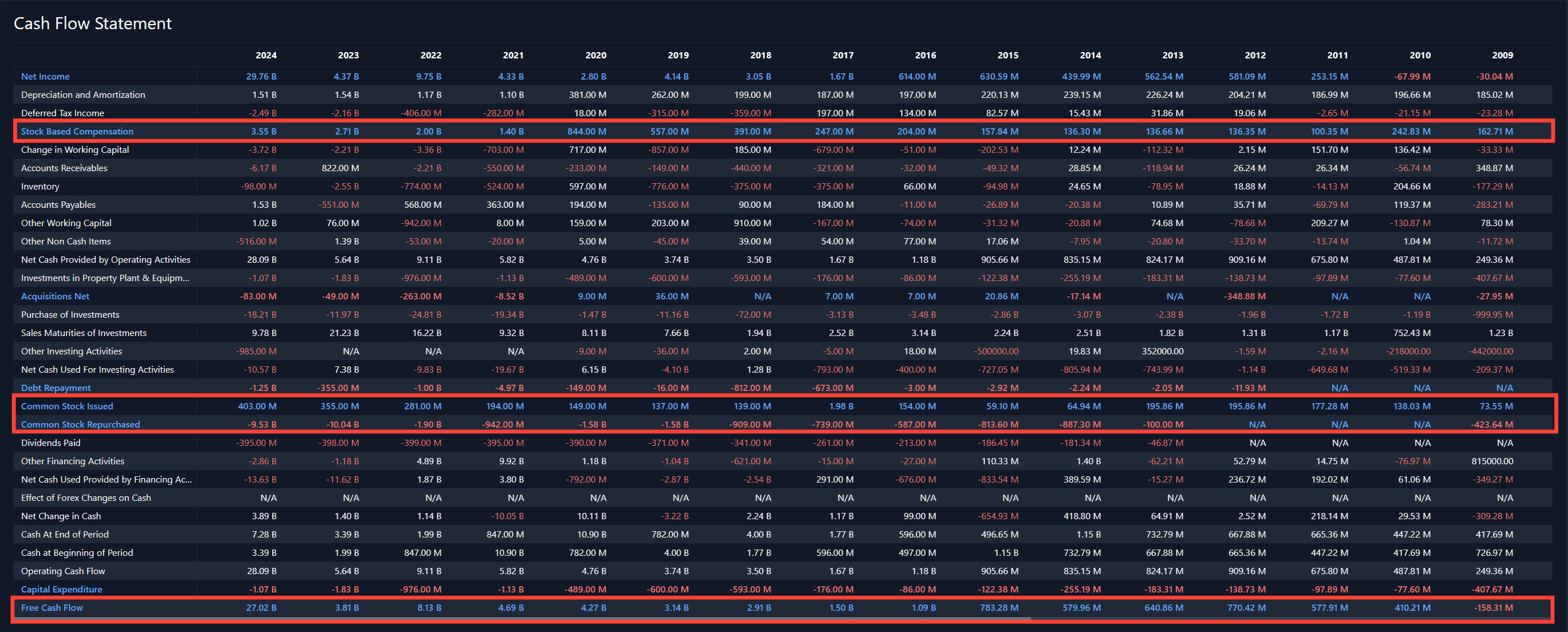

Nvidia's revenue, net income, profit margins, and free cash flow have grown impressively over the past decade. Their debt levels are also extremely manageable, which is great to see.

Things seem even better when you zoom in on the quarterly data, where the profit margins are increasing each quarter. Last quarter's free cash flow was high enough to wipe out ALL of the long-term debt if needed. NVDA keeps crushing analyst estimates every quarter, and its stock price reflects that. But that doesn't automatically make it worth its current valuation, so let's dig a little deeper.

Their capital expenditures, debt repayments, and the dividends they pay out are all easily covered by their free cash flow. The numbers would either have to be fudged or something horrible would have to happen economically to put this company at any financial risk in the near future. The company is financially healthy.

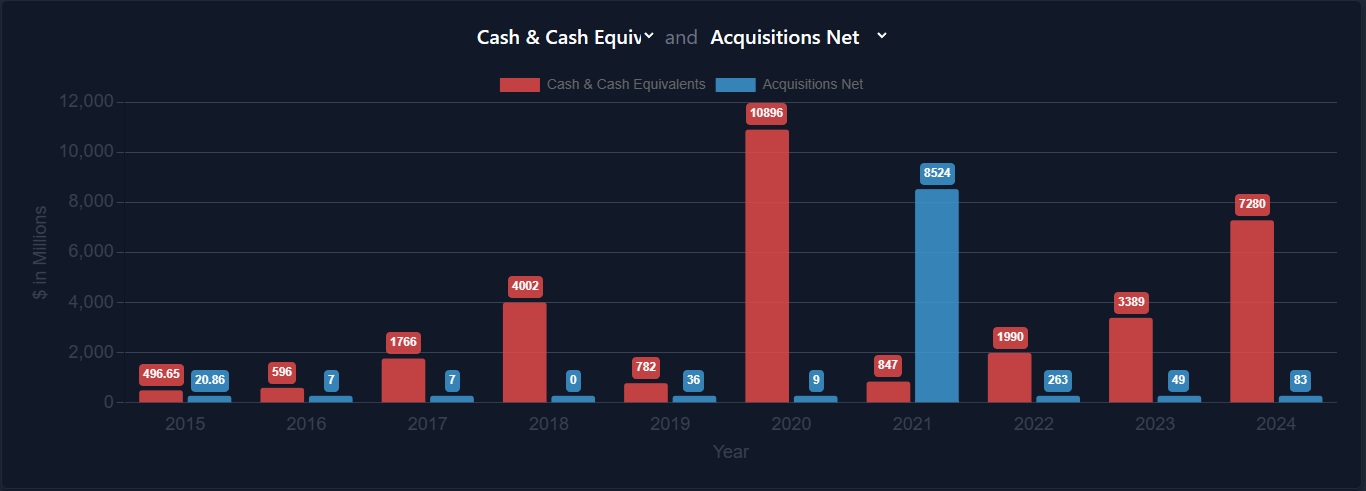

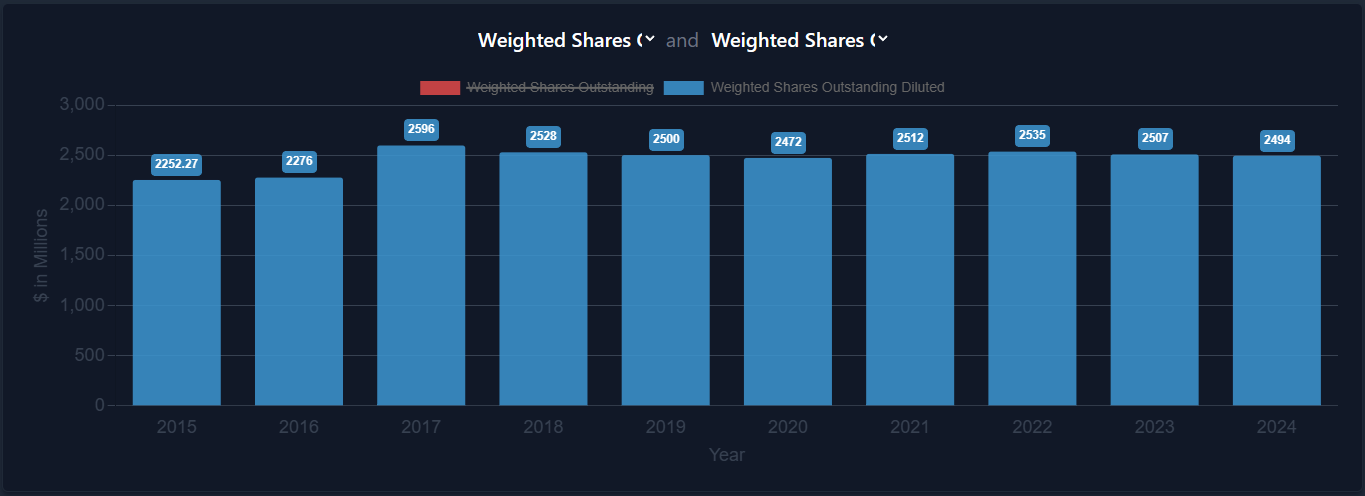

NVDA's growth has exploded over the past year, and they haven't made any big acquisitions. This shows their growth is coming organically rather than driven through acquisitions, which is really good. They have more than enough cash to cover the acquisitions they have been making, which means they could acquire with all cash instead of having to issue debt or equity to finance it, which is good! The last major thing I want to highlight before getting to the valuation models is the share count.

Their share count has been decreasing since its peak in 2017 which is also a good sign. If you owned shares in 2017 and never bought or sold any, you would now own a larger percentage of the company than you did in 2017 without having to do anything.

Buying back shares is generally a good thing but it is also situational. Doing it when the stock is cheap is one of the best uses of capital for delivering shareholder value, where buying back shares when the stock is extremely overvalued, is not a great use of capital.

Stock-based compensation is also related to the share count, which NVDA does a lot of for its employees. Let's check that out...

You can see that the stock-based compensation (which is in dollar terms, not shares) is very large. However, this, plus the amount of shares issued, is overpowered by the share buybacks, which decreases the share count.

One caveat is that the stock-based compensation should be subtracted from the free cash flow number. If NVDA was to sell the shares on the open market and then give that money as compensation it would be a cash expense so it shouldn't be treated any differently without doing the middle step in my opinion. Nevertheless, the share count is decreasing, but I think that $10 billion could be used more effectively somewhere besides buying back very expensive shares, so I am not a huge fan of that decision currently.

Price Targets

My Equity Value and Price Targets

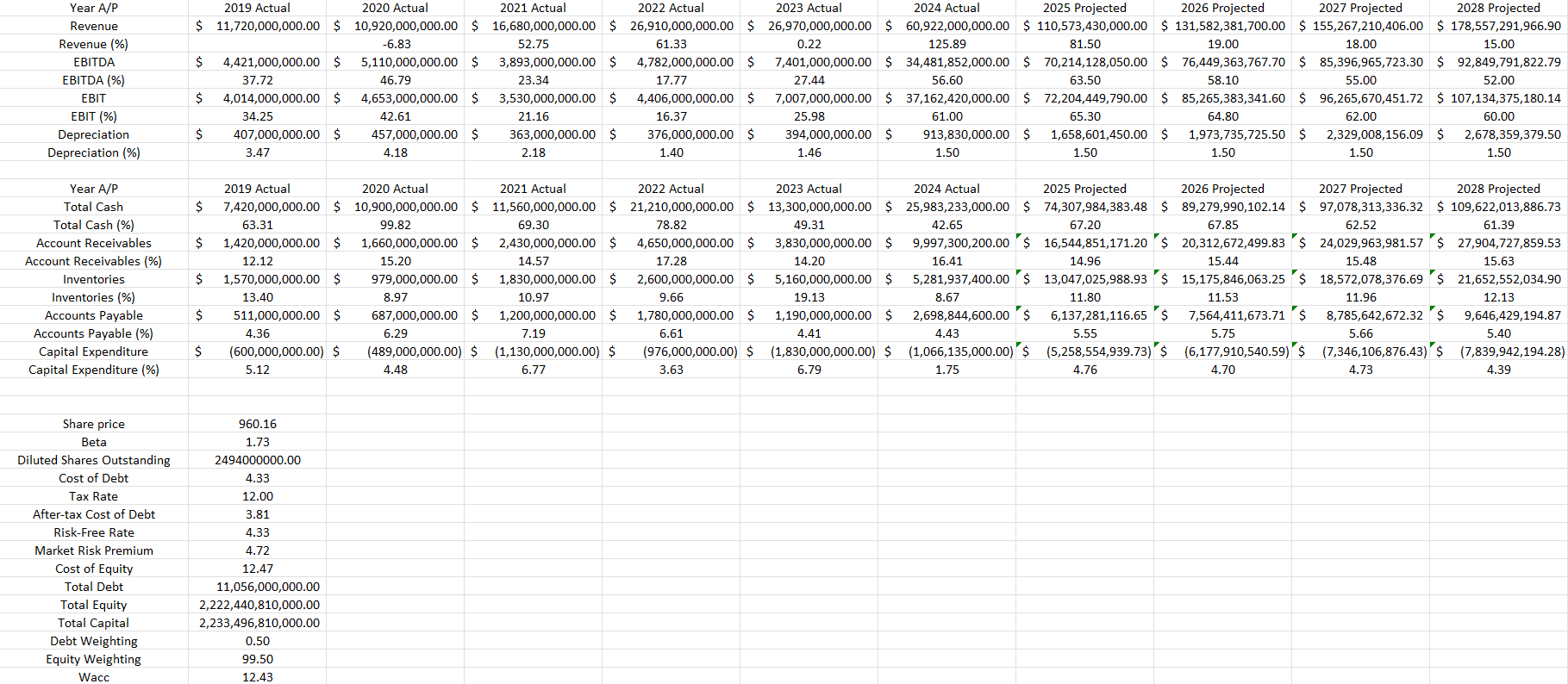

For me, the question is not if NVDA will keep growing with the AI boom, its whether or not their margins will fall back down in the coming years due to competition, which is a possibility the market does not seem to be pricing in, but we will run scenarios on that shortly. First, I am going to run a full Discounted Cash Flow Model and show all of the inputs and outputs below. I will keep the margins at their fully elevated levels.

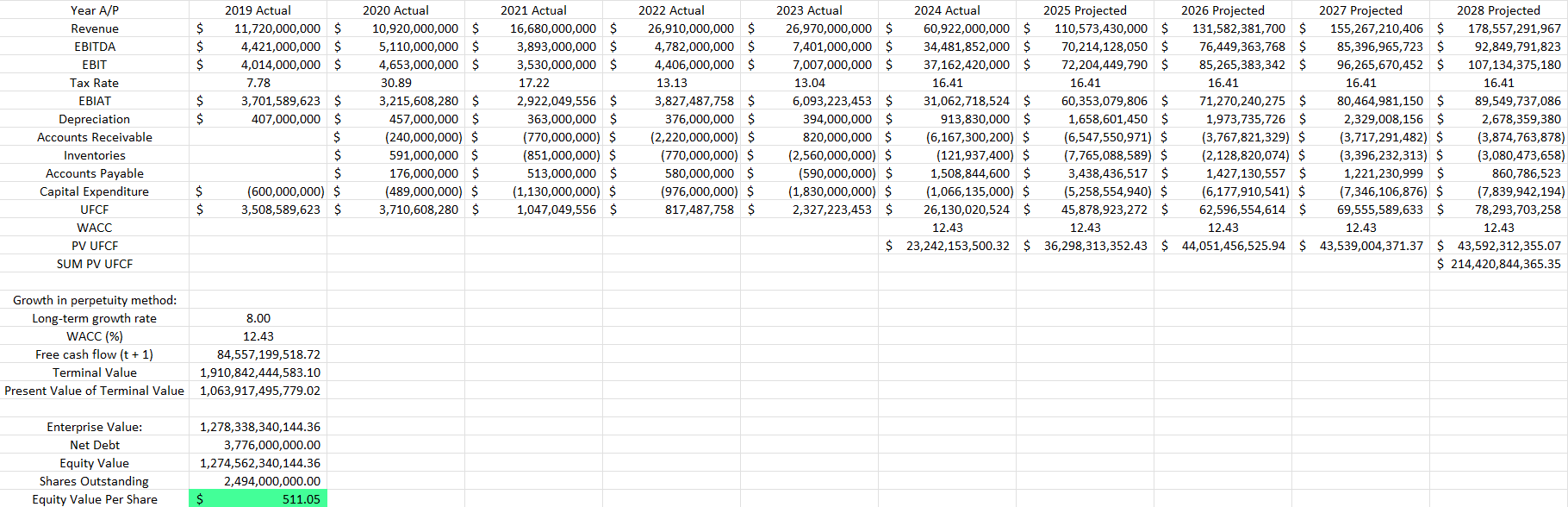

As you can see by the equity value in green, the current Equity Value Per Share is $511.05, given the specific inputs to the model and a 4-year price target of $816.57. You can change these inputs to generate any number you want, so it's important to be realistic and as unbiased as possible to avoid terrible outputs. One thing I want to highlight is that this assumed some pretty unlikely things, and it still produced a result much lower than the current share price.

For example, this assumes that NVDA's revenue grows from $61 billion in the past year to almost $180 billion in 2028. That is probably the most likely of the inputs I deem unlikely. The next unlikely inputs are the margins. This model assumes that the margins are going to increase a little and then hover around those elevated levels over the next few years, basically assuming no competition comes in and drives down margins. And the most unlikely and really mathematically impossible input is the perpetual growth rate of 8% at the end. That would mean NVDA would double its revenue every 9 years forever. When this input is lowered down to 5%, the equity value drops to $331.63 with a 4-year price target of $529.88. Therefore, according to this model, it seems as though the potential long-term return percent for me to buy and hold is very low or negative, and thus not worth it for me personally. That doesn't mean it can't go higher in the short term or that it can't perform much better than the numbers put into the model.

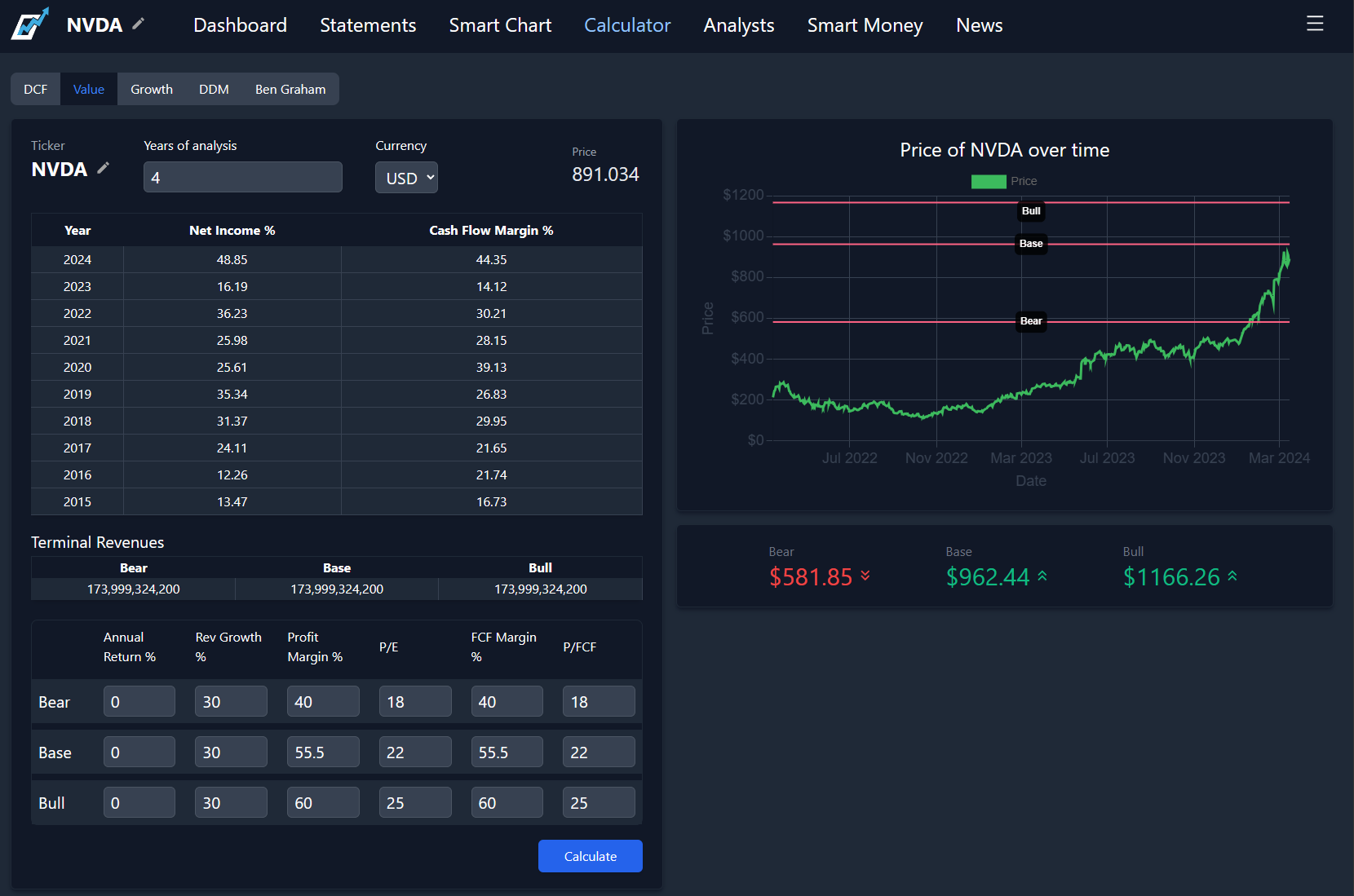

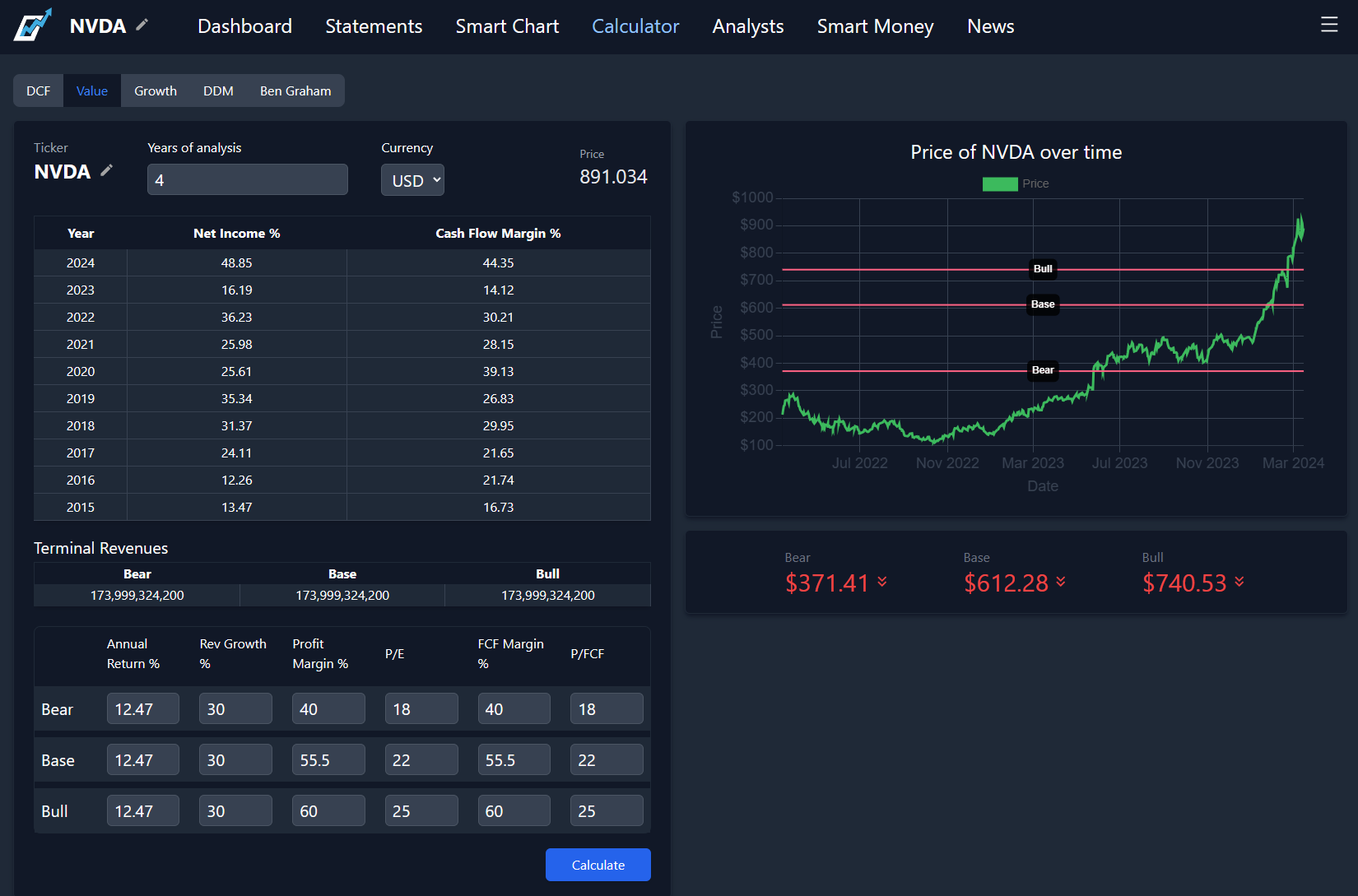

Next, I will run bear, base, and bull case scenarios using free cash flow, earnings, and an exit multiple. I will adjust only the margins and exit multiples for the different scenarios while keeping everything else the same.

Since the "Years of Analysis" was set to 4, the top image shows 4-year price targets, and the bottom image shows the prices I would have to buy NVDA at to get a 12.47% (the cost of equity) return every year for the next 4 years, assuming the model's inputs are correct.

While some of the price targets are high, the risk doesn't justify the reward at the current valuation for me personally. For the time being, I will be patient and hope that at some point in the near future, the price meets the value, so I can buy. Until then, I will explore other opportunities. As always this is my personal research and opinion and not intended to be financial advice to anyone else.

Don't forget: As a member, you also get access to our exclusive community to ask questions and share ideas, our stock analysis software, and text notifications. Click here to get started.